The High Stakes (and Critical Stakeholders) of ESG

For those not living under a rock, environmental, social, and governance (ESG) reporting has likely hit your radar. While it is becoming increasingly required by regulators in Europe, it’s (arguably) more important stakeholders asking for ESG in the U.S.: your investors, lenders, ratings agencies, customers, or employees.

-

Investors, already hungry for nonfinancial performance in corporate disclosures, are placing their bets on expanded ESG reporting: 75% say they would find value in assurance of an organization’s planning for climate risks.

-

Nearly half of consumers (48%) said they’d change their consumption habits to reduce their impact on the environment—and that’s before millennials, 83% of whom say sustainability is extremely important, take on more buying power in the coming years.

-

Studies show higher employee satisfaction scores at organizations with higher ESG scores—higher satisfaction typically leads to longer tenures and higher productivity. And those millennials we just mentioned? By 2029, they, along with Gen Z, will make up 72% of the world’s workforce. You can be sure they will be taking their talents to workplaces that support their values.

-

There are also increasing signs—as in dollar signs—that the cost of credit is lower for those who report strong ESG programs and practices. Financial instruments such as sustainability-linked loans (SLLs), for example, are bringing billions of dollars to companies that can boast strong ESG metrics, such as carbon emissions or number of women in management. Those who demonstrate better ESG scores are hauling in better interest rates.

Even the largest companies in the world are voicing their support for ESG disclosure standards ahead of official SEC actions. Apple’s call for mandatory climate disclosures for companies is among the latest—and perhaps loudest?—of the voices to enter the fray.

Given these high stakes, it has become clear that executive management teams and their boards of directors want assurance that the reported ESG data is right and audit ready.

Skeptics might be tempted to dismissively relegate ESG as "nonfinancial" and therefore not material. We would caution those skeptics and point to the recently enacted Sustainable Finance Disclosure Regulation (SFDR) mandate in Europe that effectively makes ESG material by law. Closer to home, there are the increasingly strong statements being issued by the SEC.

Between your stakeholders and regulators, you can almost guarantee that, somewhere, you’ll be disclosing information on policies, risks, and outcomes in regard to environmental matters, social and employee-related aspects, respect for human rights, anti-corruption, and bribery issues. And, to be sure, your reputation is on the line.

That’s no small task, as many companies are still living in the Wild West of ESG, where data (if it exists) is scattered everywhere and teams spend more time chasing, collecting, cleaning, and reviewing data than on the actual ESG report itself.

To be sure, ESG reporting is manual, time-consuming, error-prone, and complex. But here are some ways to untangle the intricacies of ESG reporting.

The starting is the hardest part

With all due respect to the great Tom Petty, the waiting is not the hardest part when it comes to ESG—stakeholders are asking for ESG disclosures now.

The first challenge for any ESG exercise is navigating the plethora of ESG measurement methods, frameworks, guidance, protocols, rankings, indices, and standards that are disconnected from the reporting process.

Regulatory authoritative reporting frameworks are there to help companies implement what to report and the controls needed to improve accuracy, completeness, and reliability of ESG information, including guidance on supporting evidence.

But this “help” may not necessarily serve as a beacon for those just starting on the ESG path. According to The Reporting Exchange, there are over 2,000 ESG reporting provisions by regulators, over 1,400 key ESG indicators, and over 1,000 organizations involved in the development of ESG frameworks and initiatives. You can almost be sure that individual companies will use multiple frameworks and standards and assemble multiple reports, and that the trend of combining ESG information with existing financial reporting will accelerate.

Although well-intentioned individually as standards and frameworks, when taken as a whole, this global, disjointed patchwork has grown so large that it can be counterproductive to the original intent.

To add to the complexity, companies’ business environments and reporting standards and frameworks are constantly changing. As such, one or more of its internal controls and materiality matrices may not operate as effectively as in the past and must be constantly reviewed to stay fit for purpose. It can feel like you’re caught in a hamster wheel of death.

What can be done? Harvard recently introduced an ESG reporting framework called the Impact-Weighted Accounts Initiative. It sets out to develop accounting measurements and reporting standards to translate all ESG categories into measurable currency that can consistently measure the ESG accounting impact on a company’s financial statements.

The approach is to standardize an accounting process that adds an impact measure of risk to each company’s accounting system to produce a second set of books that reflects the monetized impact of ESG efforts, rather than an ESG scoring method. This initiative is supported by the Impact Management Project (IMP).

Some work has also been done to address the framework and standard alphabet soup, including the efforts by the Corporate Reporting Dialogue’s Better Alignment Project, which has made significant progress in defining alignment.

But even with the simplest rule set, there’s still the issue of ESG data hiding everywhere.

The fragmented ESG reporting data ecosystem

With so much riding on ESG data, and its inherent complexity, we need more than just simplified rules. We need a simpler way to work—in other words, we need ESG digital transformation.

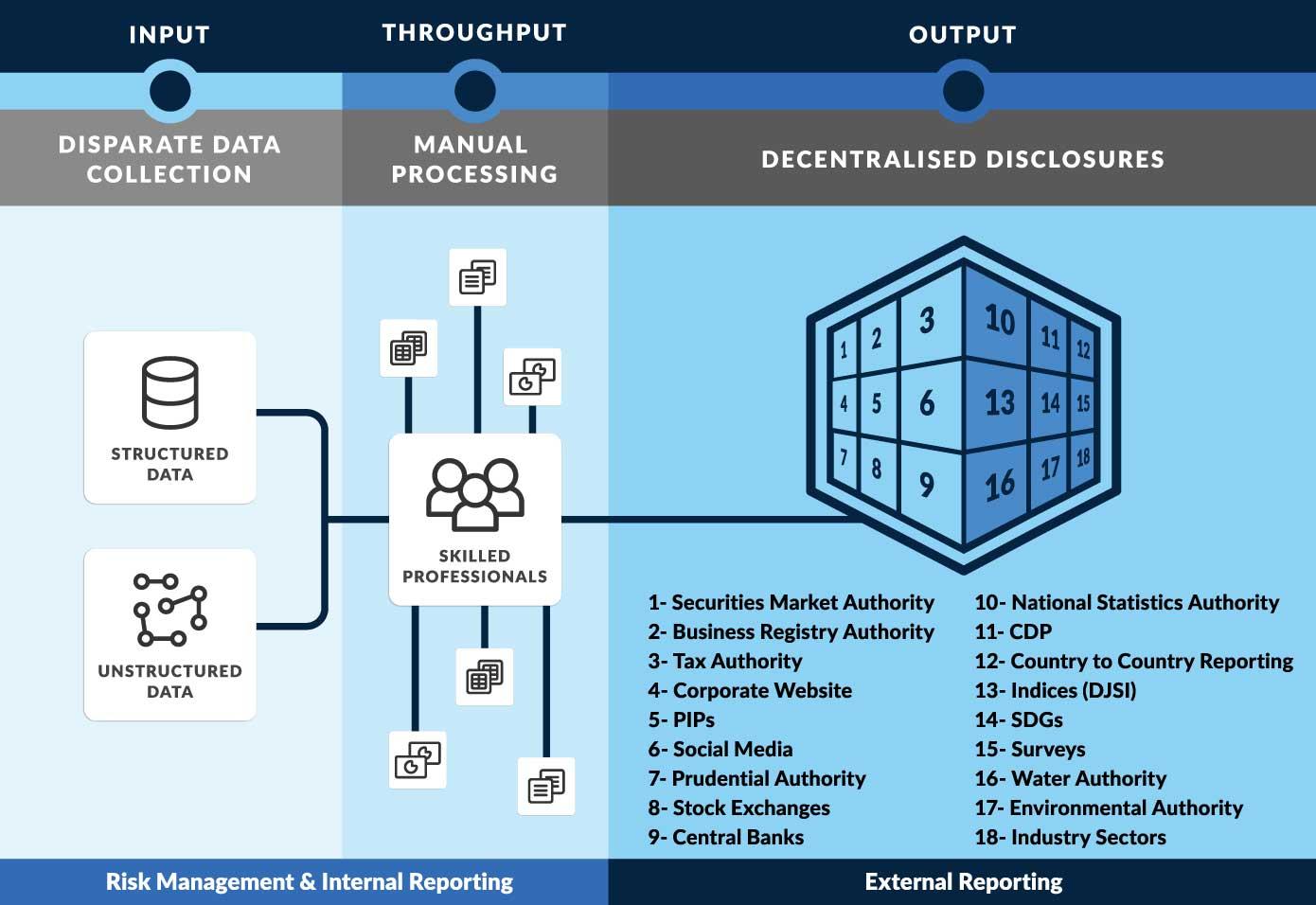

The challenge lies from trying to generate a single source of truth that can be linked to multiple disclosures and views in the ESG data ecosystem. While any transformation can seem daunting, we simplify it by looking at a three-phase data life cycle:

- Input

- Throughput

- Output

The Complex ESG Reporting Data Ecosystem:

Source: A Digital Transformation Brief: Business Reporting in the Fourth Industrial Revolution

Step 1: Input

The first step of the process is ensuring data accessibility and data availability. One of the biggest challenges is the manner of the flows and interfaces between input, throughput, and output across various systems. Plus, oftentimes the data is not captured at all in any system, causing ESG teams to search high and low for the data they are asked to report.

ESG data systems are most often not aligned and require manual effort to ensure that the output of one system is reprocessed in the necessary format to be validated for submission to multiple disclosure destinations. A well-defined purpose for collecting the data becomes essential and can help focus ESG teams on how they purpose the data, rather than solely collecting and validating information. Look for technology that can unite your many systems—or that can allow contributors to enter data directly—so you can collect ESG data at the source, instead of passing it around in unsecured and unchecked channels like desktop spreadsheets or email chains. The hard work you put in satisfying stakeholders with ESG reporting can be undone with one wrong number.

Step 2: Throughput

Once the team has ensured that the data required is accessible and available, they must ensure they meet the reporting requirements of each regulatory or voluntary ESG disclosure provision.

In this phase, the fragmentation of data types and data definitions become key challenges. Sometimes, different regulators require the same information in their specific formats or data types. Surprisingly, some individual regulators also call for the same information in different forms and in different data formats.

Data definition fragmentation can become a real challenge when reporting the same information to multiple regulators. It’s also not uncommon to find differences in interpretation of the definition of various data elements among regulators. The traditional way of assembling, dismantling, and repackaging of data in the required format can cause compliance risks.

Critical decisions are only as good as the data they are based on. Forward-thinking compliance teams must embrace good data governance around ESG data in the same manner they implemented controls around their financial reporting processes.

Again, being audit-ready is key. Look for a system that has controls over your ESG data built in. Being able to add tagging, attach evidence, gather signoffs, and refer to a full audit trail of these activities and more can build confidence in all your disclosures, not just those that are ESG related.

Step 3: Output

After the first two phases, ESG data is further connected to multiple outputs, where the need to link from a single source of truth becomes essential. With ESG and financial information will be reported jointly, you can expect that the same audit scrutiny of your financial reports will also be applied to your ESG. Find a reporting platform that gives you the freedom to create reports of all types—whether for regulatory filings or boardroom presentations—with the confidence of data consistency across the ecosystem.

In summary, the data from a company’s systems needs to be compiled and repackaged in the throughput phase in order to meet form and format requirements for ESG outputs, but the data underlying those outputs should be single-sourced and mapped against reporting outputs so that ESG disclosures are accurate, transparent, and audit ready.

Time to embrace digital transformation

More than ever, the ability to manage torrents of ESG reporting data is critical to a company’s success. Increasingly disconnected and fragmented regulatory environments make compliance overly burdensome for many companies while also inhibiting investors and other stakeholders from obtaining useful information.

In the shadows of a global pandemic—where access to quality data from remote locations is paramount to meet ESG statutory reporting requirements—the need for a solution that unifies and simplifies financial, nonfinancial, and the emerging forms of ESG data is a critical component of digital transformation.

And as mentioned earlier, unless you’re living under a rock, you’ve probably heard whispers that ESG mandates are coming in the U.S. For those who are unprepared, when ESG actually hits, it may be like a ton of bricks.

We’re closely monitoring the situation here at Workiva. As ESG continues to take shape in the U.S., we’ll have plenty more to say on the matter—including our next post on why finance is best positioned to own ESG. Watch this blog for more perspectives. Better yet, subscribe so you can get the latest perspectives direct to your inbox.

You May Also Like

Executive Summary: A Snapshot of the SEC’s Climate Disclosure Rule

Review what’s ahead in ESG reporting requirements. Plus, discover five steps organizations can take now to be ready for it.